The fate of the global economy does not rest on the US election, says Dr. Moyo. “It’s bad, whatever happens.” By Kevin Helliker.

She speaks for the left, the right, the poor, the rich, the third world andthe first. A native of Zambia, she holds a doctorate in macroeconomics from Oxford University, a Master of Public Administration from Harvard University and an MBA from American University, from which she also received a degree in chemistry.

Her résumé includes stints at Goldman Sachs and the World Bank, and she has published four best-selling books: Dead Aid, a treatise on the failure of aid to Africa; How the West was Lost, on misguided economic policies of developed countries; Winner Take All, on the implications of China’s purchase of natural resources around the world; and Edge of Chaos: Why Democracy is Failing to Deliver Economic Growth and How to Fix It.

She has nearly 1.4 million followers on LinkedIn, and more than 200,000 on Twitter. Time magazine once called her one of the world’s 100 most influential people. She sits on the boards of Chevron and 3M, having previous served on the boards of Barclays Bank and SABMiller. She’s a serial marathoner. She has visited more than 80 countries. She lives in New York and London, where she is finishing her fifth book and serving on an equal-rights panel at the behest of the British Prime Minister.

For the global economy, how important is the US election?

I don’t think the election will make a material difference to the global economy. It’s bad, what-ever happens.

What leads you to say that?

Even before the financial crisis hit in earnest this year, the global economy was in a precarious place. Large economies, from emerging markets with at least 50 million people to very large developed markets, were struggling to create growth. Most countries were failing to generate 3 percent growth—the minimum annual growth rate needed to double per capita incomes in a generation—roughly 25 years.

Add to that a lot of economic headwinds: technology and the risk of a jobless underclass, demographic shifts, income inequality, climate change, natural resource scarcity. India’s adding a million people a month to its population. Social mobility in the US has been halved in the past 30 years. Debt: Just this week the WSJ reported that consumer, business and government debt in the US had reached $64 trillion—triple the gross domestic product. Productivity—a factor accounting for 60 percent of why one country grows and another doesn’t—has fallen considerably over the past decade in developed markets, in an era when technology should be leading to increased productivity. Finally, there is impotent public policy. We have been living in a period of negative interest rates, massive debt, massive government deficits and enormous, and arguably unsustainable, welfare systems.

Again, that is all before COVID.

“We’re beginning to learn a sharp lesson about the societal cost of private freedoms. Tradeoffs are going to be required of us. Tradeoffs much more challenging than simply wearing a mask.”

I’ve been very fascinated by the similarities between the Gilded Age of 1870 to 1900 and the one between 1950 to 2008. Both were periods of high economic growth, globalization, and the rise of very strong and important corporations. Both periods had very notable widening income inequality. Both were periods where you had relatively weak or small government in terms of government being an economic participant as an arbiter of capital and labor. A data point worth considering: From 1850 to 1900, all US presidents except Ulysses S. Grant had one term in office—only one. They were actually broadly considered irrelevant.

That first Gilded Age was punctured by World War 1, the Spanish Flu and the Great Depression.

What followed was a 20-year period of low economic growth, deglobalization through protectionist policies on trade and the breakup of large corporations. You had government become much more important both in terms of size and economic importance. You get FDR and his three terms as president. He builds the New Deal to address income inequality. The turnaround really came from the War, ’39 to ’45.

One marker I think is interesting: The Dow Jones Industrial Index peaked in 1929 at 381 points, and it did not hit 381 again until the 1950s.

If you believe that history repeats itself, then we will be going into a period of low economic growth and big government. On big government, Angela Merkel has talked about the idea of 7/25/50. That Europe is 7 percent of the world’s population, 25 percent of GDP, and 50 percent of world welfare payments. If you add the US, you’re talking about 12 percent of the world’s population, 50 percent of GDP and 90 percent of the world’s welfare payments. If you consider that 90 percent of the world’s population lives in the emerging markets—this is an imbalance that’s, longer-term, unsustainable.

Now there is an impetus for more tax revenue, because governments need it, and also more regulation that becomes more anti-trust. Corporations will likely get smaller. We have had a period where all the large sectors—banking, technology, airlines, pharmaceuticals, energy companies—are dominated by a handful of companies. We essentially very organically have ended up with a number of oligopolies.

Every aspect of globalization is now unwinding. The area of trade in goods and services. The movement of capital is being subjected to capital controls. The movement of people, immigration is a political third rail, and there is a risk of a splinternet—that over the next decade the world will split into China-led versus US-led technology platforms. Lots of barriers are being put up.

The result, if you look at forecasts, is that projected equity returns materially have come down from, around, 8 percent-plus to between 4 and 6 percent.

To use the unofficial motto of the pandemic, what should developed nations do to build back better?

The answer has to be more efficient government. As I wrote in my last book, economists and business people can do all they want in terms of enhancing efficiencies. But if you have government that is ineffective—that’s not only not doing constructive stuff but is actually hurting the business environment—then you’re not going to grow or generate long-term returns.

Mike Bloomberg has talked about there being four things that government needs to be. It needs to be data-driven. It needs to be forward-leaning. It needs to focus on measured outcomes. And it has to be not corrupt. If you have that type of government, you’re off to the races.

But we don’t have that type of government. And we don’t have the sort of imaginative thinking that really was the bedrock of the United States. There’s no Manhattan Project. There’s no DARPA. There’s no large-scale government-led effort as was in thebuild-up of Silicon Valley. When the American Civil Engineers releases data showing that America gets a D-plus in terms of infrastructure, there’s not a response, not a state or federally led program to rebuild the interstates or highways. At best public policy appears reactive, and not proactive.

“In 20 years’ time, what do I know for sure is going to be important? Two things: China and technology.”

To what extent is the future of the global economy in the hands of corporate executives?

I would say it isde facto, but notde jure. Especially in the West, there’s a clear delineation between public policy makers, the private sector and civil society. Traditionally corporations have not been charged with providing public goods such as healthcare, education and infrastructure, or as involved in socio-cultural debates. However, society, as well as large institutional investors and regulators are increasingly demanding that corporations take a stand in these areas.

Several years ago, I wrote an article talking about how I expected these lines to be much more blurred, not least because of what China has done. China, many people would say, has been quite successful running an economy where these lines are blurred. Of course, there are lots of arguments saying that we haven’t yet seen the costs of China’s choices, and that day will come, et cetera. But for now, they’ve been able to do this.

In a surreptitious way in the West, companies have been taking on the responsibilities of government not only in terms of social goods like education and healthcare, but also areas like climate change. And now this has been sort of formalized because of the Business Roundtable statement, and the move away from the Milton Friedman view of corporate responsibility. I believe this will continue to a far greater extent in years to come.

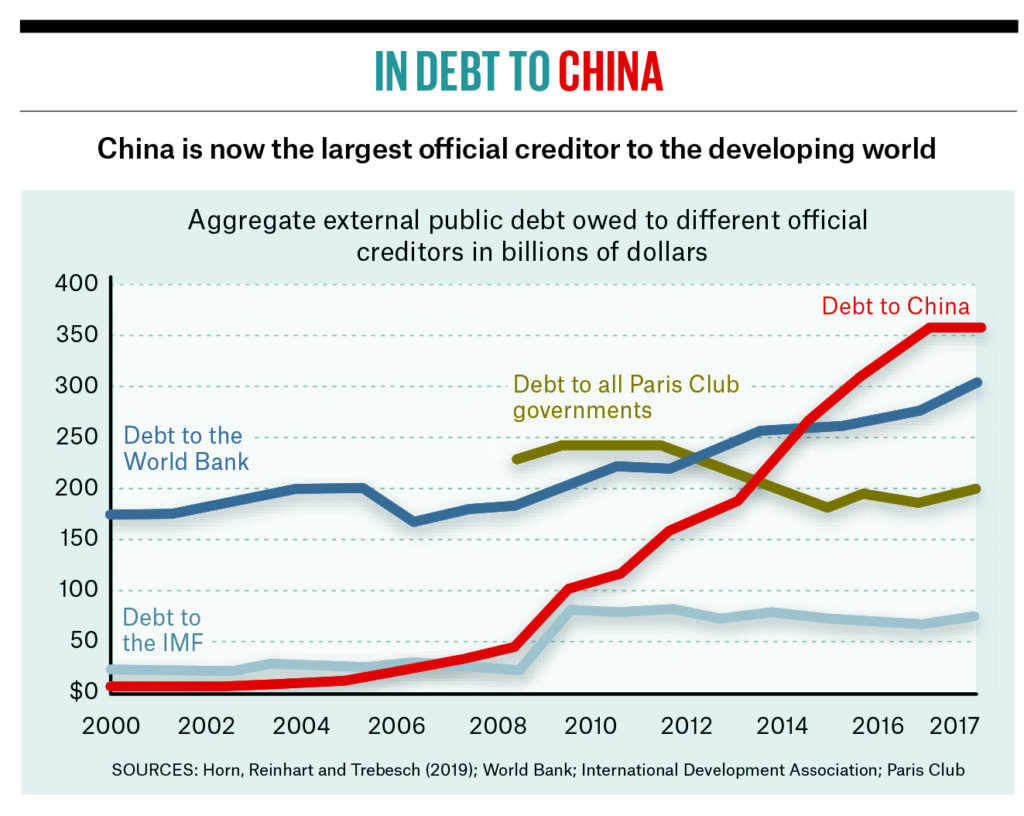

In a recent tweet, you noted that of each of the G20 countries except China has suffered a recession this year. Will the pandemic have the effect of enhancing China’s global presence?

There is a risk that that happens. I would point to three trends that are becoming solidified in this COVID era. One is China trading with emerging markets and other countries. They are stamping their imprimatur on global trade—now as the primary trading partner in many of the largest emerging and advanced economies.

Similarly, in foreign direct investments, China is not only the largest lender but often the largest investor in many large economies around the world, from Australia, across Europe, South America, and Africa.

The third thing is that China is now the largest lender in terms of debt to the emerging markets. It’s actually surpassed the G20 and some of the multinationals. China is thought to be buying distressed debt on the secondary market and then forcing governments to negotiate by giving assets instead of restructuring the debt. That’s really important to China’s continuing efforts to become a much bigger player. Additionally, China is the largest foreign lender to the US government—fluctuating between No. 1 and No. 2 with Japan. Naturally, this means debt is not merely an economic variable, but also a mounting geopolitical concern. As we speak, China is in the middle of selling off the US Dollar debt, which is why there’s been so much weakness in the dollar recently.

In 20 years’ time, what do I know for sure is going to be important? Two things: China and technology.

In our last interview, you said, “All my life I’ve been raised to believe that democracy and market capitalism are the path to economic growth, better living standards, and reducing poverty. However, with China’s legendary economic success and democracies in advanced countries struggling, people around the world are no longer convinced, perhaps because we who believe in democracy are no longer convincing.” Has the pandemic—which China arguably handled better than the West—affected that dynamic?

At the heart of that question is ideology, meaning: At what point are the costs of ideology so great that we turn into pragmatists?

When we last spoke I was talking about countries that are very poor getting to the point where they say, “Democracy all sounds nice on paper, but I need to eat today.” Westerners love their freedoms. I can do whatever I want. I can have as many children as I like. Nobody’s going to tell me that I can’t eat as many burgers as I want to.

We’re beginning to learn a sharp lesson about the societal cost of those private freedoms. Tradeoffs aregoing to be required of us. Tradeoffs much more challenging than simply wearing a mask.

What is your latest book and when is it out?

It’s out spring 2021, and the topic is corporate boards. It’s cryptically titledHow Boards Work. [Laughs] It’s actually the closest thing I’ve written to a memoir, because I talk about my experiences on boards.

It’s not a big exposé. When there’s a corporate scandal, people will say, “Where was the board?” I’m trying to provide some clarity around what levers the board has, and what a board’s mandate is. What exactly can a board do? Why can’t it do more? How should we be thinking about that?

It really tries to address a handful of basic questions on matters like worker advocacy, data privacy issues, how to engage in a world that’s become deglobalized, how to manage supply chains, how to tap into global talent. I end the book by offering proposals on how boards can better do their job, which is to support management while also checking and challenging management.

Also, make sure the trains run on time. In a climate where scandal gets all the attention, we tend to forget that hundreds of millions of pieces of clothing, goods and services are delivered every single day, in an efficient, cost-effective and sustainable way. That’s done with the oversight of effective boards. I’m offering ideas for how we can make boards even more effective given all the transitions and challenges of the global economy and geopolitics.

While writing your book, you’re serving on a UK government panel?

I joined the Race Commission, under the Prime Minister’s office, and I’m chairing its Employment and Enterprise subgroup. They approached 10 of us, none of us politicos, across the political spectrum, to look at the data, objectively look at the evidence, and come back withsuggestions.

All four of Ms. Moyo’s books made The New York Times Best Seller list: Dead Aid, Winner Take All, How the West Was Lost and Edge of Chaos. The last, released in 2018, addresses popular uprisings in a period of anemic economic growth and widening wealth inequality.

Has diversity and inclusion truly been a concern of boards and corporations? Or has it been just lip service?

I’ve been supported throughout my career by a lot of people who don’t look like me. But one data point does not make a trend, and for way too long there absolutely has been a lot of systemic racism.

Corporations, and society more generally, have to be more ambitious. Giving a check for $10 million to some community program—that’s motherhood and apple pie. That’s necessary but not sufficient if we’re going to jumpstart society in a more inclusive way.

When I sit in boardrooms during discussions on this issue, I try to push management to be more aggressive and innovative. I figure, “We can put a man on the moon. And so why can’t we solve these types of problems?” The challenge we face is twofold. First, we’re extremely impatient. The world we’re living in is an artifact of long-term challenges that need long-term solutions, like investments in education. And people don’t have patience for that.

The other issue is, I want to make sure that the result isn’t a few people who look like me winding up on boards and in the C-suite. As long as Black people and other minority groups don’t have the tools to enhance their lives, then there is a serious, systemic problem. Everybody deserves the right to fully participate in the economy, to have equal access to capital, to opportunity. That, to me, is the rub.

I worry that we could be in a world now, with cancel culture and other agendas, where people are using injustice to fight injustice. As a consequence of that, you’re seeing many more companies going private. If capital accumulation, capital formation, investment in everything from technology to pharmaceuticals—if that more and more happens privately, there’ll be less likelihood that people like myself can participate in the economic enhancement of the future.

I want to make sure that the conversations are constructive, they’re helpful. Minorities need feedback. I don’t want a situation where people are scared to give me feedback because I am a Black woman.

Unfortunately, given the multitude of and manifold challenges facing the global economy, I think there’s a real risk that the social justice issues slip to the bottom of the agenda again. If COVID numbers spike up and global growth goes down even further, you could get more political populism, and that could move social justice further down the agenda.

Do directors face new pressure to advance the interests of all stakeholders?

In terms of the corporate mandate, we’re there on behalf of financial shareholders. The Delaware incorporation rules talk about directors being there on behalf of shareholders.

But in the real world, where there’s a lot of public failure in the delivery of public goods, schools, infrastructure, health care, etcetera, corporations are being required to participate in broader societal advancement not only through regulation but by investors and other stakeholders—employees, customers, the communities in which we work. The 2019 Business Roundtable statement on the purpose of corporations solidified this view.

Those of us on boards are straddling this line, making sure companies remain profitable enough to fund R&D, innovation and future proofing—while making the world a better place. My book talks at length about navigating that. We don’t want the pendulum to swing to where we’re all “woke” but no longer focused on making sure the business is viable.

Meet the authors

-

Partner

New York

Kevin joined Brunswick in early 2017 as Editor of the Brunswick Review. In 27 years at the Wall Street Journal, he covered politics in London,…

More from this issue

The WFH Issue

Most read from this issue

Above the Fray

Targeting Untruths

You might also like

Self-Driving Boats Powered by AI & Clean Energy

Mike Rowe Talks Shop