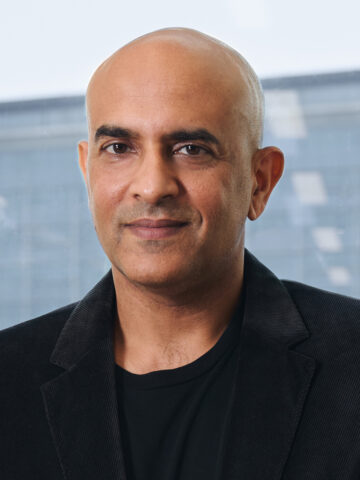

From a small office, Uday Kotak built the leading full-service financial institution Kotak Mahindra Bank. We spoke to him about his journey and prospects for investment in India. By Brunswick’s Khozem Merchant and Pavan Lall.

Uday Kotak’s first job in a bank was running one. As founder and first CEO, Kotak’s namesake creation, Kotak Mahindra Financial Services, swiftly embraced and embodied India’s national aspirations. Kotak was one of the first recipients of a banking license when reforms set India onto the path of a freer economy, and he can claim a modest role in the country’s transformation. On September 1, 2023, shy of three decades at the top, he stepped down as CEO. Today he is a billionaire and Asia’s richest banker.

The business, now Kotak Mahindra Bank, remains a strong performer, matching its founder’s status as an exemplar first-generation risk-taker in a nation of young, restless risk-takers. The bank has flourished into a full-service financial institution with a market cap of more than $40 billion built on operations in insurance, broking, fund management, asset management, retail banking and corporate banking.

In a wide-ranging conversation with Brunswick’s Khozem Merchant and Pavan Lall, Kotak reflects on India’s vibrant financial system, the way forward for the country’s capital markets, why India’s conglomerates might feel home-market opportunities trump global ones, and on his own new role, as the founder and leader of a newly minted family office.

When you started the bank, where did inspiration come from and whom did you turn to for counsel?

I was straight out of business school and was fascinated by finance, so my father supported me in starting a business and gave me a small 200-square-foot office space to operate out of as opposed to working for someone.

There was a huge but imperfect market: the state owned 97% of the financial sector. Back then a saver would deposit at 6% or 7% and the banks would lend at some 17% as per regulation. You had top corporates who would borrow at 17%—my idea was to give the borrower less than 17%. It was a simple model with a spread between 6% and 17% and the idea was to buy and sell at 12% and 16% instead. While it seemed straight forward, no one was doing it through a bill of exchange instrument. The state was fine doing this for large companies because they needed capital for growth. It was simple.

I would say I bounce ideas at a lot of people but mostly it is important to be a sponge and be open to absorbing ideas and learning and eventually make your own framework of principles.

Having spent a lifetime in banking, how are you examining business opportunities now?

We looked at our family structure to decide that. I have two sons, one of whom is working with the bank and the other is in the US working for Amazon. Within Kotak Mahindra Bank, the family owns 26% which is the largest single-family ownership in the banking space. I had three roles earlier: board governance member, manager and strategic shareholder. Now I continue to be on the board of the bank and some committees but in a non-executive capacity. I have shed my role as a manager.

We (the Family Office) are looking at investing in the US as a part of our diversification and to broad base our interests. That means we would look at non-financial service businesses in the US. We are also looking at non-financial services in India and across the world. If there is something that doesn’t conflict with our financial services holdings, we will do it. When I was CEO of the bank, I was very clear about even remotely getting into any conflict areas. Business Standard for example, the newspaper the family owns, was entered into before the bank started. Now, as a matter of philosophy I am free.

“The biggest business opportunities don’t require the most capital.”

Tell us about USK Capital?

Uday Suresh Kotak Capital is our family office. We have been low-key about it—no website, nothing on the internet. It’s about the transfer of intergenerational wealth and you will see that over the last 15 years many mid-sized families have led the creation of institutions as family offices.

It doesn’t excite me to make gains on equities and trading, but what has excited me is an owner’s mindset without the need for a quick exit. An owner’s mindset means a timeline with a long horizon unlike a private equity player who wants to sell a stake and make an exit in, say, five or seven years. That’s not to say that we will never sell a business, but our view will be long term.

That is how we built Kotak Bank, which was started as a business where my family put in Rs13 lakhs out of a total capital of 30 lakhs ($40,000 in those days).

Over the last few years Kotak stock has had an impact on transition as it moved from founder CEO to professional management. That’s how I think a financial services business needs to be built. Take JP Morgan or Morgan Stanley, where the founders are gone but there is an intergenerational connection to managers via the foundation of trust and long-term commitment to creation of value. That’s our thinking on business.

Has the time come for Indian companies to be truly global—and are we better insulated now from global economic shocks?

I think it’s still early days. India had its tryst with internationalization in 2008 with the likes of Jaguar Land Rover, Corus and Novelis [acquired by Tata and Aditya Birla Groups]. Then things went quiet for a while. We need to be real on two counts. Some 65% of the world’s market cap is in the US, which only accounts for 26% of global GDP. The second is that India may be the fifth-largest economy but if you look at per capita income it’s still at around $2,400 dollars, so our denominator is both a challenge and an opportunity.

We are not entirely insulated but our macro-economic factors are in good shape. I had a big group meeting with global pension funds and other investors and the big question that comes up is “at what value?” A lot of people are looking for strong value propositions independent of China; so, yes, there is positivity but that’s the query that comes up.

What important regulatory shifts are you observing in the Indian capital market, for example, around bond market reforms?

I think there’s a major transition happening. Broadly in the world of financial intermediation there are two models: the saver-borrower model, which is the more cautious one, and the investor-issuer one, which is the market securities model and includes asset management and so on. In the investor-issuer model, capital is transmitted directly, so both the upside and downside go directly to the investor. In the saver-borrower one, the saver’s funds are protected by a wall of capital in the middle. Both are prevalent in India but there is a shift happening to the investor-issuer model which has a much lower financial intermediation cost but with higher risk transmission, as is the case with anything that is high gains.

Is more regulation coming? I’d liken it to roads and vehicles. Of course, we need good traffic signals and laws with good highways, we need to be careful we don’t have so many traffic rules so that no one drives at all. Getting the balance right is not easy, but it is key.

“India has a chance to get to the level of maturity the US has but hasn’t been tested yet.”

Of course there’s a downside to too much regulation as well.

Yes, to say we want zero accidents is also a risk for growth. You can’t stop accidents but good regulation will minimize them. What’s more important is, how fast can you resolve an accident? An example is the blowup of Silicon Valley Bank in the US, which was swiftly resolved. Frankly, that’s the one country that got the investor-issuer model right. In most economies, accidents linger because it requires a significant maturity of the investor class as well as the political economy.

Financial reforms sit on a tripod: first is regulations, then the market players, and thirdly the fisc, which is the state, but distinct from regulation. How you ensure seamless thinking across regulations while keeping in tune with the market, means the challenge there is verticalization.

On the second leg of the tripod (practitioners and players), we need to bear in mind that a lot of Indian investors are first timers and have never seen a downturn. Coming to debt and bond markets the issue with debt is it’s taxed as interest income where the highest marginal rate is 39%. On the other hand, the highest marginal rate on capital gains for equities is 12.5% and so policy still encourages equities and real estate over debt. In essence, if an individual puts funds into a bond he or she will be taxed at 39% whereas real estate or equity will be 12.5%.

Third, with regard to the country’s fiscal health, the challenge is balancing the interests of regulators, market players and government policy makers, aligning them to create sustained growth toward a $35 trillion economy in the next 25 years. That’s the vision.

There are some shifts to capital gains tax occurring, but at this stage there’s a massive amount of retail that has woken up to the pleasures of equity but haven’t ever seen the pangs. That movement is itself a big structural change to the financialization of the economy and is good for lower intermediation costs. But it requires sophisticated policy making and political economy and a maturing of the investor class. If things tomorrow go wrong, God forbid, millions of retail investors who found they were getting high returns and safety will have to realize that high returns come with high risk.

India has a chance to get to the level of maturity the US has, but it hasn’t been tested yet.

What are some ingredients needed to ensure our financial markets land well, long term?

There are 16 IPOs happening this past week alone. Sixteen. So my personal view is a high quality supply of paper. It’s also a great opportunity for the government to divest stocks they own at high valuations.

There’s a general opinion that India’s capital markets are overheated but you’re of the view that we are not near a bubble peak?

I said that in February [2024]—and the market is up since then, of course. No one can predict when it is peaking. I had said the market is getting bubbly but not near a full bubble which is undoubtedly happening now.

What would you advise a young entrepreneur today with regard to investing?

There’s so much more capital today versus when I started and there’s also much more opportunity—but I also think the biggest opportunities don’t require the most capital. It’s about getting the opportunity right. The trouble is that opportunity never announces itself when it’s there.

Meet the authors

-

Partner, India Office Head

Mumbai

Khozem has more than three decades’ experience in media and business in India and the UK. He specializes in Indian macro and public affairs and… -

Director

Mumbai

An author of books about white-collar crime and Indian tycoons, Pavan is a former journalist specialising in coverage of big business in India as well…

You might also like

Lighting the Future

A Vaccine Expert on Miracles, Misinformation and Missing Data