Governments and private enterprise must work together to solve the “trilemma” of a just energy transition, says Brunswick’s Maxim Petrov.

Energy is the lifeblood of the world economy, powering our daily lives and economic activities. Recent events, from Russia’s invasion of Ukraine to widespread energy shortages and rising inflation, have underscored the strong political and economic urgency to reconsider how we think about that lifeblood.

The transition to lower-carbon energy sources has become a policy priority around the world, including in Asia. China leads the way in renewable investment and electric vehicle infrastructure, accounting for almost $550 billion, or nearly half of global spending, according to data from Bloomberg New Energy Finance. The US was in distant second place with $140 billion spent in 2022, while the EU totaled $180 billion as a single bloc.

But that spending says nothing of the far greater challenge: creating an equitable and inclusive transition away from fossil fuels toward low-carbon and climate-resilient societies.

Such a large-scale transformation must ultimately benefit all segments of society, particularly the vulnerable and marginalized populations around the world.

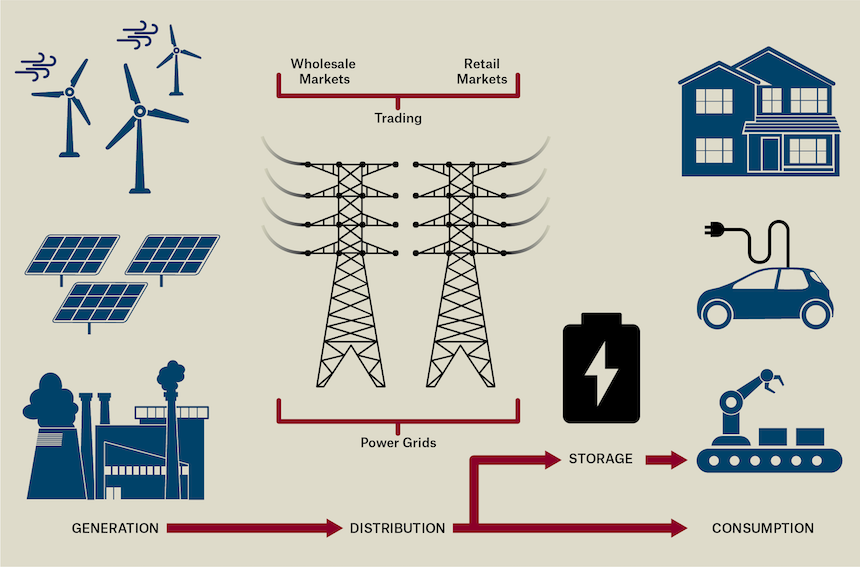

The industry calls this the “energy trilemma,” highlighting the importance of balancing energy security, affordability and environmental sustainability. These three dimensions are often interrelated, yet provide a simple, effective framework for policymakers trying to understand the complex trade-offs involved.

This is particularly significant in Asia, where different regions may not transition at the same pace. Moreover, energy solutions designed in the West or in north Asia may not emphasize the same elements as those in developing Asian countries.

Southeast Asia is widely considered the next global economic powerhouse. Its population of over 660 million is expected to reach 800 million by 2060. Almost every ASEAN member state, except Cambodia and the Philippines, has committed to net zero by 2050. However, according to the IEA, the region’s energy demand is set to grow at around 3% annually until 2030, with three-quarters expected to be met by fossil fuels.

EDP Renewables, the world’s fourth-largest renewable energy producer, is investing $7.5 billion through 2030 to establish a leading clean energy hub from its regional headquarters in Singapore.

“There is undoubtedly a structural market opportunity in Asia, given that the region is expected to account for 50% of global energy consumption and 40% of global renewable capacity additions until 2030,” says Pedro Vasconcelos, Chief Operating Officer of EDP Renewables Asia-Pacific. “In the short term, developers need scalable market opportunities, clarity on long-term transition plans and greater visibility on routes to market. Without these elements, renewable adoption will not progress as quickly as society requires.”

The more advanced economies in Asia are leading the way, Vasconcelos says. “Today, our growth strategy is focused on Singapore, China, Japan and South Korea as they have deep potential and stable regulatory environments. Developing nations are following suit, but they will require additional regulatory alignment and cross-border interconnectivity to unlock Southeast Asia’s clean energy potential.”

In the case of Indonesia and Vietnam, abundant coal reserves and untapped natural gas resources mean that fossil fuels continue to offer a more cost-effective and reliable energy source, slowing the transition to greater renewable energy adoption. Andrew Harwood, Research Director at energy research firm Wood Mackenzie in Singapore, says governments view renewables as just one part of the mix.

“When your energy demand is growing in mid-single digits, it’s hard to just rely on solar and wind, especially when what you really need is stable base-load power to keep the lights on,” he says. “There are other, non-commercial factors involved in policy decision making.”

These factors include reliable job creation and utilization of existing fossil fuel infrastructure. Phasing out coal has been a common strategy in developed nations where coal was already a diminishing economic factor. But aging, less efficient coal power plants in the US and Europe contrast with those in Southeast Asia, where the average age is just under 11 years old. Retiring these plants before they have fully achieved their return on investment could result in up to $100 billion in stranded assets across coal and gas infrastructure in Southeast Asia, a severe blow to the region’s economy.

Ideally, the energy focus for Southeast Asia should be on creating a green economy with quality jobs, opportunities for reskilling and upskilling workers, and avenues for new and foreign capital into the region, all while minimizing the negative impacts on traditional fossil fuel sectors, Harwood says.

To meet its climate goals, the region needs to invest $180 billion per year into clean energy infrastructure through 2030—six times the region’s average annual spend of $30 billion over the past five years.

Europe and the US have shown that government subsidies and state guarantees can be instrumental in accelerating the transformation of energy systems. They have introduced tax incentives, reduced regulatory uncertainty and mitigated the social costs of the transition by stabilizing energy prices. Ambitious initiatives like Fit for 55, RePowerEU and the carbon border adjustment mechanism have accelerated decarbonization efforts across Europe. In the US, the government has spurred the growth of solar and wind power, green hydrogen and carbon capture and storage. The Inflation Reduction Act has been a game-changer, attracting substantial investments in clean technologies as developers rush to establish operations and bring their capital into the country.

For less affluent, developing economies in Southeast Asia, the situation is more complex. Many governments in the region lack the financial resources, regulatory expertise and political resolve to develop new, affordable, low-carbon energy supplies.

“When your energy demand is growing in mid-single digits, it’s hard to just rely on solar and wind, especially when what you really need is stable base-load power to keep the lights on.”

One potential solution is to leverage public-private partnerships to drive investments in clean energy projects, reducing the financial burden on governments while mobilizing private capital to support the transition.

This is exactly what the $20 billion Just Energy Transition Partnership program in Indonesia aims to provide. The international initiative was announced at the G20 in November 2022 and is being led by the US, Japan and Europe. The objective is to raise half of the funds from the public sector and half from private investments, using the proceeds to retire existing coal plants earlier and invest in renewable energy projects.

Regional cooperation can also help facilitate the shift. Singapore recently began importing up to 100MW of hydropower from Laos via Thailand and Malaysia, an ambitious cross-border deal involving four ASEAN nations. Although other initiatives like the Australia-Asia PowerLink Project ultimately did not materialize, this serves as a valuable starting point and crucial test for similar programs.

“In addition to utility-scale solar in Vietnam, we are pushing for project developments in wind and batteries, while exploring cross-border opportunities in Malaysia and Indonesia. In other markets, like Thailand and the Philippines, we are attentive to regulatory changes that welcome and incentivize foreign direct investment,” says Vasconcelos.

A more localized approach will also be an important component of the transition strategy regionally. Decentralized and community-based projects can provide affordable and accessible power to remote areas while also promoting local economic development and fostering a sense of ownership among communities.

Finally, governments are being encouraged to prioritize education and training programs that empower local populations to participate in the green economy. The International Labour Organization estimates that while Southeast Asia could potentially lose less than half a million jobs in fossil fuel industries by 2050, it could gain up to 5 million jobs in the renewable energy sector. The creation of that skilled workforce will require policy support and private sector incentives but would simultaneously drive momentum toward a more sustainable energy economy.

The challenge of solving the trilemma, creating a truly sustainable low-carbon energy future for Southeast Asia, will require all of these strategies and more. But success will ensure a greener and more prosperous future for all of its citizens.

More from this issue

Southeast Asia

Most read from this issue

Binge Empire

LKY The Musical

You might also like

AI Bearing Fruit

The Endurance Entrepreneur