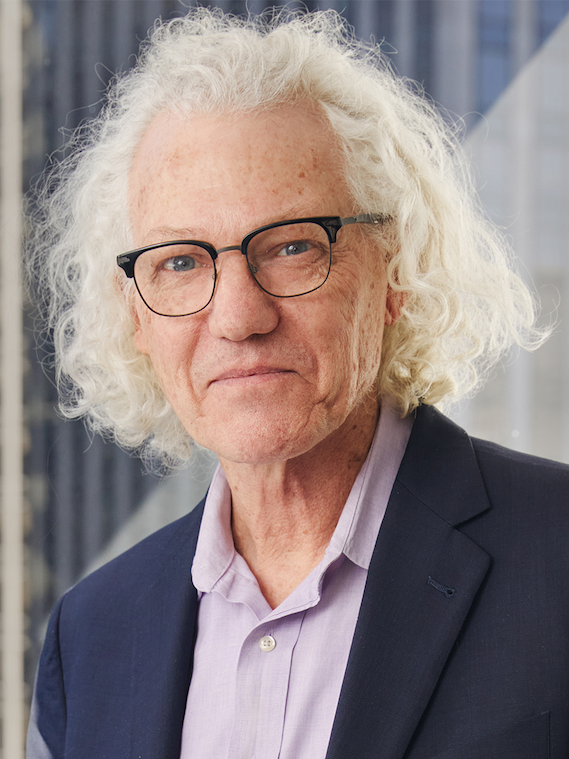

Rishi Khosla, the Co-founder of leading neobank OakNorth, talks about serving the “missing middle” of enterprise and the role that segment plays in society. By Brunswick's Alice Gibb and Carlton Wilkinson.

OakNorth bills itself as a service “built by entrepreneurs for entrepreneurs.” Launched in 2015, the fast-growing London-based digital bank focuses on helping growing businesses that are not being well served by commercial banks.

True to that motto, the vision for OakNorth emerges directly out of the entrepreneurial experience of Co-founders Rishi Khosla and Joel Perlman. In 2002, the partners co-founded their first startup, Copal, a data and analytics company servicing the financial sector.

“Joel and I started working together when we were 26 and 27,” Khosla says in a recent conversation with Brunswick Review. “We built Copal up, and then went straight into OakNorth.”

At a critical moment while building Copal, the pair needed a debt vehicle and found that commercial banks didn’t see them as a worthy applicant. Despite being profitable, having a good cash flow and an enviable client list, they were turned down at each bank. Eventually they gave up on their modest loan request and turned to an institutional investor for a much larger amount in the form of a dividend recap, allowing them to grow into a formidable business. In 2014, with global operations across 13 markets and 3,000 employees, they sold to Moody’s. A decade on, the business is now under private equity ownership and is more than three times the size it was when it was sold.

“It was that experience, while we were building Copal, where we saw how bad commercial banks really were,” he says. “We just said, ‘You know what? We can do this better.’ And here we are. We’re trying to do this better.”

OakNorth serves a broad base, but its ideal customer is that familiar category of an emerging business with large ambitions—what Khosla called the “missing middle” of enterprise.

“You’ve probably heard the stat a million times about 99.9% of all UK businesses are SMEs [small-to-medium-sized enterprises],” he says. Collectively SMEs form the backbone of the global economy. While most generate less than $1 million in revenue a year, some are much larger and merit special consideration.

“We commissioned some research last year from the Social Market Foundation, which found that those with $1 million-to-$100 million turnover collectively represent just 1% of all SMEs, but 8% of all SME employment, and 22% of all SME turnover,” Khosla says. “So that just gives you a demonstration of the outsized impact of this category. Their demands are those of larger companies, but clearly the economics are not the same as larger companies. Therefore, they don’t get the same type of attention from banks. They get underserved and overlooked.”

“It was that experience, while we were building Copal, where we saw how bad commercial banks really were. We just said, ‘You know what? We can do this better.'”

Commercial banks, Khosla felt, were hampered by a rigid, slow evaluation structure built on banking processes essentially out of step with the digital era. OakNorth was designed to fill that gap, providing fast, flexible debt finance for emerging businesses that needed it. A “neobank” backed by SoftBank, among others, it has no bricks-and-mortar outlets and no baggage of the legacy banking infrastructure to weigh it down. And the experience of Copal gives OakNorth an advantage in data analytics capabilities, particularly as they apply to credit markets.

“We spent 12 years prior to OakNorth building a data analytics business,” Khosla says. “That business had 3,000 people when we sold it, approximately half of whom focused on credit. What we’ve done at OakNorth is really take that learning around credit and credit markets and build that into a whole framework. That enables us to apply the large cap lending approach to smaller companies. Today, that whole data theme very much runs through everything we do.”

The pace of growth for OakNorth has surprised even its founders and it is now the leading neobank in the UK and has begun lending in the US.

Born in the UK, Khosla’s father was also an entrepreneur and kept his son beside him as he followed opportunities, allowing Rishi to experience different cultures and watch the ins and outs of building a business firsthand from a very early age.

“My father had a friend he went into business with, in Tehran of all places,” Khosla says. “The revolution broke out. We moved to India, and my father went back and forth from Tehran. Then we came back to the UK. When I came back to school here, I used to speak Farsi, Hindi and English in one sentence, which made it slightly challenging for anyone to understand me.”

Well ahead of his age group at school, he eventually earned a masters degree in accounting and finance at the London School of Economics at only 20 years old, and accepted positions first at ABN AMRO Bank and then GE Capital. He also managed a private equity venture portfolio for Indian steel magnate Lakshmi Mittal, one of India’s wealthiest business leaders, and became an early investor in PayPal.

At the London School of Economics he met Joel Perlman, a native of Colombia who had studied at Georgetown University. Perlman went on to work as a Consultant at McKinsey before partnering with Khosla to launch first Copal and then OakNorth.

In the following conversation, we spoke with Khosla about the challenges of launching a business and how serving other entrepreneurs in the “missing middle” of enterprise serves society as a whole.

“Entrepreneurialism sort of runs in my veins,” he says.

At the 2024 World Economic Forum in Davos, Khosla spoke on a panel about AI governance.

With the goal to help this category of SMEs, why start a bank versus a venture capital firm?

The service gap that we identified—the missing middle—is the gap to get debt as a growing business. It was very much around debt funding, not equity funding. The alternative business model for us would’ve been to set up a direct lending fund. A fund vehicle is a very efficient way to build a business, but in a business cycle, there will always be times when the market for raising fund money dries up. That may not therefore have the same longevity and scalability as a bank vehicle.

Now, with hindsight, I would say both models have proven effective—there are a lot of direct lending funds that have been able to scale through the years, to very large numbers. But you also have, on a percentage basis, many more funds that don’t. Our approach of getting a banking license meant that we could do that more consistently. Yes, we’re subject to a lot of regulation, but that regulation is rightly placed because you are bringing consumer deposits into the equation, as part of building a robust business that can survive the test of different cycles and the like. So that’s what fundamentally drove us to make that decision.

Given the fast growth of OakNorth, does the label of “neobank” still apply?

Absolutely. Ultimately a neobank, at least how we look at it, is a bank which is built on fundamentally a digital architecture, using modern technology, not using legacy technology. Whereas when you look at traditional banks, they have web technology as a layer, but underneath they’ve got a lot of legacy pumping through. In our short history—eight and a half years since launch—we’re already on our third refresh of our tech stack. That’s the level at which we’re investing and continually moving forward from a technology perspective.

You have more flexibility?

A lot more flexibility, therefore we have the ability to service customers in a much more delightful manner and give them the tools to enable them to self-service.

In terms of the scale of our ambition, if you look across all the other neobanks which are being set up, they’ve mainly focused on the consumer and micro-SME space. We’re very focused on the missing middle. That segment hasn’t been targeted by any of the other neobanks.

If we look at the experience that we deliver to our customers, versus what traditional commercial banks deliver, it’s dramatically different in the same way that a consumer app delivers a different banking experience for customers at an incumbent bank. It reinforces our position as the go-to neobank within the commercial segment.

“We went from, at that time, $100 million lent to $350 million by the year-end—literally, within a matter of six months.“

Do you feel you’re a “first mover” in this space?

I would absolutely say we are. In the customer segment that we’re talking about, as far as we can see, we’re one of the only movers. At the moment, the competition is coming more in the form of the incumbent banks trying to up their game. And I think that’s healthy.

Data analytics is central to your business model. What role does AI play and how has that expanded as the technology has exploded?

We started off with statistics. We went from statistics to machine learning. Now, we’ve gone from machine learning to experimenting with GenAI.

How much was AI truly part of what we did from day one? Not at all. In 2017, 2018, we started bringing in machine learning. Those days, most people would use the terms ML and AI interchangeably, but it was really ML—not AI. Today, there are absolutely places where we’re using GenAI. But again, I would say we’re experimenting in many more places than we’re actually using it.

What we do is split the economy into 274 industries. And for each of those industries, we’ve got both the ML model and the fundamental model, which work together. That gives us a forward-looking view of those industries, which enables us, as we get a new potential client, to create on the fly a forward cash flow model of that business, and we do that across our whole loan book on a monthly basis. That’s what enables us to underwrite more rigorously, but also then monitor and manage positions in a much more rigorous manner.

What were the biggest challenges in getting OakNorth off the ground? And what, now, are the biggest challenges that you have, given the scale that you have achieved?

In terms of getting it off the ground, like with anything, you launch and suddenly—nothing happens [laughs]. You expect this whole rush of everything to come towards you, and nothing happens. Doing a zero to one is always incredibly hard.

We launched in September 2015. June 2016 was the Brexit referendum vote. That ended up being a catalyst for our business because most other lenders stopped lending.

We went from, at that time, $100 million lent to $350 million by the year-end—literally, within a matter of six months.

In terms of a current challenge, you’re always thinking steps ahead in the business. How do you continue to deliver for your customers as you get more and more scale, how do you make sure that you don’t slip and slide back into the experience of one of the traditional banks? The thing we try to do is look ahead as much as we can and try to be ahead of the curve.

It seems that some of the “S” in ESG is served by that business model. How do you implement ESG generally?

Oh, you’re exactly right. When we started the business, we said to ourselves, if we’re successful, we will have a positive impact on society because we’ll be helping the most productive part of the commercial world get the capital they need to grow. The segment that we focus on generally has the highest productivity, and is responsible for the most GDP and employment growth in any community.

We’ve always taken the approach of being socially minded. That doesn’t mean we’re a social enterprise, it means that we’re minded just to act appropriately with suppliers, customers, employees, et cetera—to do the right thing for them. Those two things have been integral in building OakNorth.

Beyond that, we’ve also contributed to societies that we’re operating in through philanthropy. We formalized our commitment in 2018 where we donate 1% of our group profits to supporting charitable causes and socially minded business. A couple of years ago, we added 1% of our team’s time as well. We call it our 1+1% Commitment. Those have always been very consistent themes that fall under “social.”

When it comes to the governance bucket—try getting a new banking license and building a bank without good governance. It’s the only way to operate and survive.

When it comes to the “E,” we decided in 2019 to understand our position from a climate perspective. We reached net zero for Scope 1 and 2 emissions by purchasing offsets, and then through 2020, we started building our climate risk frameworks.

Since then, every year we’ve been looking at our carbon footprint, including finance emissions and have ambitious targets to reach net zero for Scope 3 emissions by 2035. In the interim, we’ll continue to use offsets, while we rely on them to a lower and lower degree. Offsets aren’t the goal. They’re a transition which we feel are better than not doing anything. We want our carbon footprint to reduce, but while we’re reducing it, we offset.

What does the 10-year plan look like?

We built the business in the UK, and we license some of our software in the US. In the latter part of last year, we also started lending in the US and we have ambitious growth plans there.

We started OakNorth to solve the access-to-capital requirement for the missing middle—businesses with $1 million-$100 million turnover—but we’re now widening our offering to provide full banking services, along with our analytical toolkit. We intend to help those companies not just do their day-to-day banking, but also get better metrics on their business and run their business more effectively.

This under-served middle segment is a global problem, so on a 10-year basis, we will absolutely be looking at other geographies, but the US and UK will still represent the majority of the business.

Meet the authors

-

-

Director

New York

Carlton Wilkinson is a Brunswick Director and Managing Editor of the Brunswick Review, based in New York. He is an award-winning journalist, a music educator,…

More from this issue

Transformation

Most read from this issue

Charting Biden’s Climate Course

Macron and the Olympics

You might also like

China CheckUp

Quantum Visionary