Few would know better than Tim Adams, President and CEO of the Institute of International Finance, whose members span 60 countries and include the most recognizable names in the industry. His answer: Technology.

The health of the US banking system in the aftermath of the collapse of Silicon Valley Bank; the state of US-China relations; proposed regulation from the Federal Reserve; financing the climate transition—these are the topics on which leading media outlets have recently sought Tim Adams’s views.

The demand for his perspective reflects how uncommon is its blend of breadth and depth. For the last decade, Adams has led as President and CEO the Institute of International Finance (IIF), which lists its members as “commercial and investment banks, asset managers, insurance companies, professional services firms, exchanges, sovereign wealth funds, hedge funds, central banks and development banks”—essentially every player in modern finance.

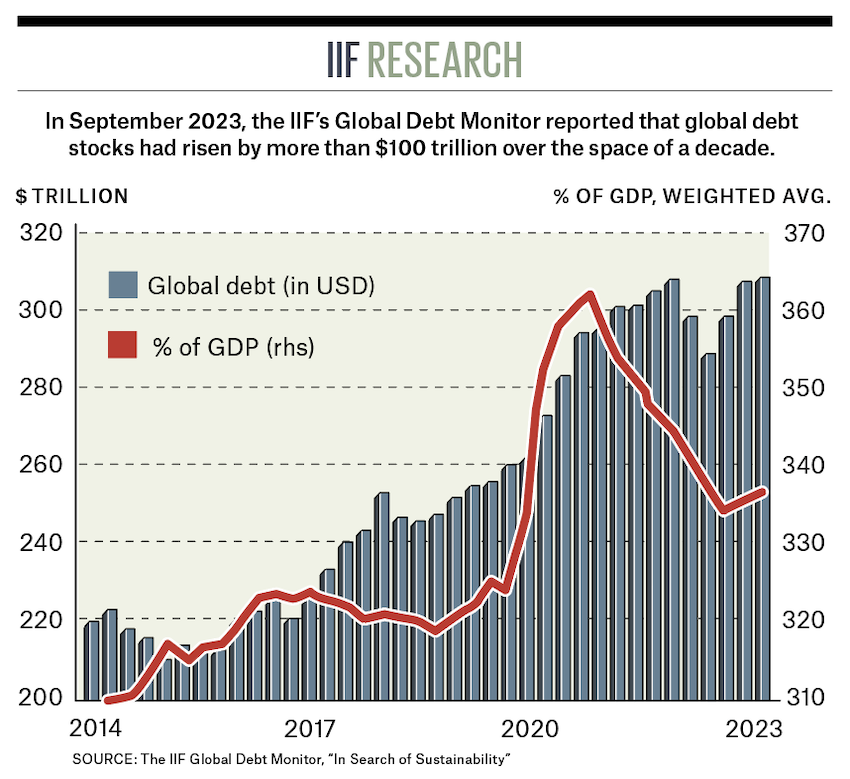

Headquartered in Washington, DC, the IIF has offices in Beijing and Brussels, Singapore and Dubai. Its 46 board members are an all-star cast of global finance leaders. The IIF’s research—particularly on capital flows and debt levels—regularly attracts global media coverage, while its events are among the most reputable in the industry.

Before joining the IIF, Adams was Managing Director of a global economic advisory firm, and had served as Under Secretary of the US Treasury for International Affairs. He had also been Chief of Staff to two US Treasury Secretaries: Paul O’Neill and John Snow.

Brunswick Partner Molly Millerwise Meiners spoke with Adams in late summer to get his views on everything from AI to ESG, “woke CEOs” to smart regulation. The interview took place just before Adams was set to get on a plane. Accompanying him on his travels was a reading list that seemed fitting, but not exactly relaxing: a stack of books on artificial intelligence, and a just-released 1,000-plus-page proposal from the Federal Reserve.

For better or worse, how has the global financial system changed over the last decade?

It’s been an incredible time, joining the IIF after the Great Financial Crisis and at the early stages of the Basel III process—which, it’s remarkable we’re still talking about implementing.

Without question you’ve seen greater financial inclusion, particularly in emerging markets. More people have access to a range of products and services to save, to invest.

And there’s been a technological revolution. We went from thinking about banking as a physical structure with tellers, to actually banking through our smartphones and apps. Whether it’s the front-end and the customer experience, the way the back-office operation works or the way in which you do credit scoring, we’ve automated and employed the latest technology.

We’ve also seen another revolution: the green revolution and an embracing of sustainability. While this is divisive in the US, so many other jurisdictions are moving ahead quickly. For the global economy to make a transition to a low-carbon or decarbonized world by mid-century, estimates are we’ll need anywhere between $2 trillion to $6 trillion annually. Wherever that money comes from, it’s going to be intermediated through financial institutions or capital markets, so our industry will play a huge role in the shift toward a more sustainable global economy.

“You cannot stay in business if you don’t listen to your customers or investors. You can’t attract the best talent if you don’t understand their values.”

Is that one of the reasons the IIF lists sustainable finance as a top priority?

There are a large and growing number of business opportunities for our member firms in this space. If a $100 trillion global economy is going to transition to a different energy mix at a historic pace, you’ve got to pay for it. And the financial services industry writ large—capital markets, insurance companies, banks, venture capital—are instrumental to intermediating the trillions that are going to be necessary.

Just think about the IRA [Inflation Reduction Act] here in the US and how transformative it could be, should be, and probably will be. Finance will play a massive role in facilitating the federal funding across the associated industries that will feed into it.

If you look globally, it is an unstoppable process in which most of the advanced world and most of the emerging world is moving—not in lockstep—but toward a collective objective.

Companies, particularly in the US, are walking a fine line with elected officials and policymakers when it comes to ESG. The right is accusing companies of “woke capitalism” and the left is pushing companies to go further. How can companies navigate this difficult landscape?

I’ll start with climate. I think it’s really about being honest with all parties, and saying it’s a transition. Jamie [Dimon, CEO of JPMorgan Chase] and other leaders have talked about this. We’re going to need fossil fuels for decades to come. If you look at the IEA [International Energy Agency] or the IPCC [Intergovernmental Panel on Climate Change], they assume and expect a continued reliance on fossil fuels for decades.

It’s not a cliff effect. It is a transition, and it has to be a just transition. There are 10 million people in the United States employed in the fossil fuel industry up and down the supply chain. You have states like Texas that get $20 billion a year in taxes and royalties from fossil fuels. The idea that you are going to turn something off tomorrow is fanciful thinking. We need to tell both sides that it’s not the scary thing they think it is.

More broadly, there’s an enormous amount of exaggeration of the phenomenon that’s described as the “woke CEO” who’s imparting their personal political values in the DNA of their organization. Does it happen? Sure. The corporate sector is huge. But by and large, what you see are leaders across the industry wisely thinking through and listening to their investors, employees, customers, suppliers and partners. They are looking at this in a broader sense of capitalism. As Brian Moynihan [CEO of Bank of America] said: It’s about profits and purpose.

You cannot stay in business if you don’t listen to your customers or investors. You can’t attract the best talent if you don’t understand their values. Each firm is part of a different ecosystem with a different set of values, and they, the C-suite, need to reflect the values of that system.

I’ll use my two teenage children as an example. They won’t buy products from companies that don’t reflect their personal values—if supply chains use forced labor, or if materials aren’t sustainable, they won’t be a customer. There are companies that are going to appeal to them, and there are going to be companies that say, “We don’t want your business. We’re going to appeal to someone else.” To me, that’s just the market economy at work.

And ESG, the term which has become so incredibly electrified that now people don’t want to use it, is just a metric. It’s a tool to measure the risks embedded in many of these firms and an understanding of that risk on the balance sheet. As an investor, I want to know what those risks are. Again, this is capitalism at work—empowering investors to know who and where and how to invest. That’s the heart of a market-based system.

It’s unfortunate ESG has become demonized, and that the political system has decided to weaponize it in a way that I think benefits no one. In fact, it distracts from some real issues we need to grapple with.

Speaking of issues—what are your takeaways from the collapse of Silicon Valley Bank and the surrounding crisis we saw in the financial sector? What’s the right remedy moving forward?

Going back to your first question, about how the world has changed in 10 years—we’ve added trillions of capital, trillions of liquidity to the system. We’ve stress-tested it. The banking system—and IIF represents more than just banks—is different than it was during the Great Financial Crisis thanks to greater regulation, greater oversight, more muscular supervision. It’s more robust and hardier, and that’s what we witnessed in February and March.

There were a couple of days there I thought, “OK, this is a real-time stress test.” And the system came through with flying colors. The firms that had problems were idiosyncratic business models. Each had a unique story, which I think in retrospect reflected a firm that wasn’t well run or supervised.

When you have 4,700 banks in the United States and four of them end up not performing well, we need to focus on the fact that the system worked. And the system worked globally. You have 11,000 banks that are a member of SWIFT [Society for Worldwide Interbank Financial Telecommunication; a global financial messaging network]. If you have a broad definition of financial institutions, there are over 30,000 institutions globally. They all opened for business and continued to lend.

My concern is a few idiosyncratic institutions and the Basel process are being used as an excuse for a broad-based, and fairly aggressive, set of regulatory changes. That’s puzzling and a bit of a disconnect. And if that’s what the Fed wants and the FDIC wants, they should just be explicit about it. This isn’t about Basel. This is about something a whole lot more.

We need to empirically evaluate these different proposals on a cost-benefit analysis, and they should implement what makes sense. But I think some of this is driven by the false narrative that capital requirements are the solution to every perceived problem. And some of the problems they’ve cited weren’t the problems that have been touted.

“While technology is keeping [CEOs] up at night, it’s also a great opportunity. This is a truly revolutionary time—and not just for our industry, obviously.“

You’re connected with CEOs across the industry. What issues are keeping them up at night?

Technology is always a point of discussion. How should they think about cyber-resiliency and cyber-intrusion? That’s a constant battle. Some individuals, state actors and non-state actors are all looking to penetrate the system and institutions. It’s an arms race, and institutions are spending billions to try to stay one step ahead of the bad actors. And on top of that they have to layer geopolitics. If you’re a Swedish or Finnish institution and your countries have joined NATO, might you be concerned about Russian retaliation? Those concerns—technological, geopolitical—are ones we hear about frequently.

Leaders are also talking about their technology spend: What are they spending on? How do they ensure a good ROI? How do they spend their technology budget in a way that allows them to compete not only with competitors, but also other technology platform companies that now provide financial services or financial intermediation? This is especially critical as so much financial intermediation is occurring outside of the regulated banking system.

So it’s an arms race both on the offensive—staying ahead of the criminals—and defensive. How do you ensure you have the latest and best technology? You’re seeing major banks spend $10-plus billion a year on tech. But what if you’re a mid-tier bank or a smaller institution? How do you keep up or compete? How do you provide the experience that customers want because they are used to the great services they get on their apps today?

And then there’s the pace of change. If you go back to January at our board meeting, we really didn’t talk about ChatGPT or AI. But over the last four months, I’ve toured the world over and found AI to be the number one topic among CEOs. Just keeping up with the issue of AI, particularly Generative AI like ChatGPT, has become a full-time job.

The regulators themselves are also struggling to keep up with AI because of its black box attributes. You can’t back test it. So, the people who supervise and regulate it, as well as the industry, are all struggling with how to embrace this technology. How do we put it to work? How do we afford it? How does it integrate with our current legacy systems? What are the pitfalls? What are the guard rails?

So, while technology is keeping them up at night, it’s also a great opportunity. This a truly revolutionary time—and not just for our industry, obviously. Those who can navigate this, spend wisely, pick the right technologies and implement them in an efficient, effective way are going to be the winners.

Meet the authors

More from this issue

People Puzzle

Most read from this issue

The Cyberneticist

Dambisa Moyo

You might also like

Above the Fray

Engine of Progress