A larger perspective reveals growing investor pressure on the underlying issues. By Brunswick’s Pru Bennett and Rory Macpherson.

As the debate around ESG has become increasingly politicized and co-opted to suit partisan narratives, the concerns that the term encapsulates remain undeniably at the heart of conversations around strategy happening in boardrooms all over the world. Such concerns occupy a necessary aspect of decision-making related directly to investors’ perceptions of the company’s financial prospects.

In this regard, it is worth stepping back from the arguments to take in a larger view: where the ESG concept came from, why it has become fundamental to the investment process, and why now, more than ever, it remains an important topic for the boardroom.

Key Drivers & Turning Points

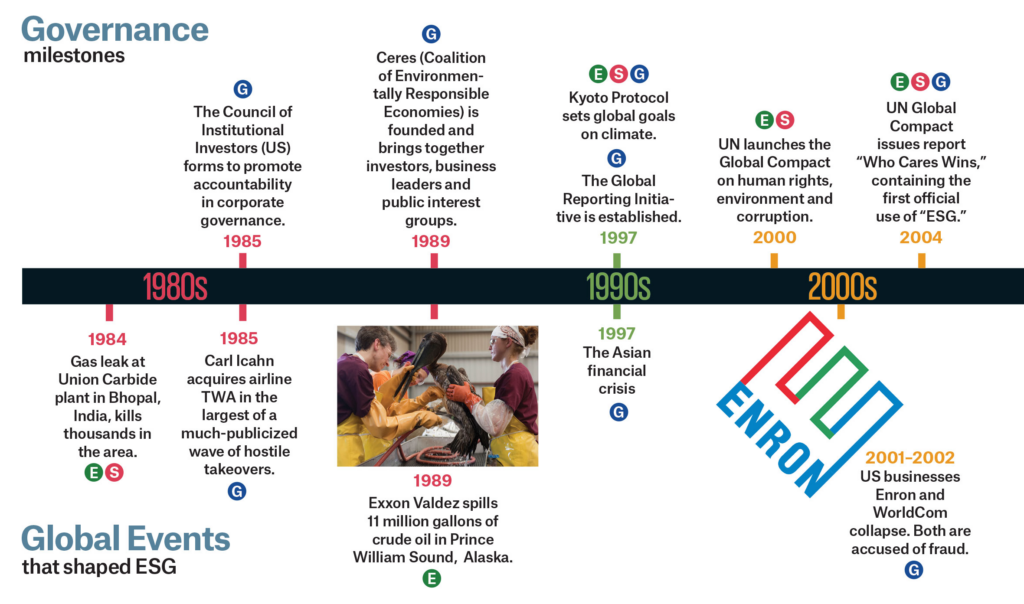

While religious ethics and social movements have advocated for responsible business practices since at least the 17th century, socially responsible investing gained traction in the 1980s, driven by concerns about business governance, environmental degradation, human rights abuses and corporate scandals. The stage had been set in the 1960s and ’70s, when public outcry over pollution and the dangers of chemicals such as DDT, which had been deemed safe by the industry, led to the formation of the Environmental Protection Agency in the US.

In 1984, the Union Carbide chemical disaster in Bhopal, India led to thousands of deaths, yet was just one of a number of significant high-profile environmental and social disasters that arose during the decade, additionally causing damage to both reputation and market value. These, in turn, resulted in a broad push by both investors and civil society for companies to be financially responsible for costs that had previously been borne by external stakeholders.

In 1985, in response to a wave of so-called “greenmail” payouts—in which minority shareholders threatened a hostile takeover to force leadership to buy back shares at a premium—a handful of public employee pension funds banded together to form the Council of Institutional Investors. Also in 1985, Bob Monks founded proxy advisor Institutional Shareholder Services (ISS) with the goal of helping asset owners carry out their fiduciary obligations in a thoughtful and informed manner.

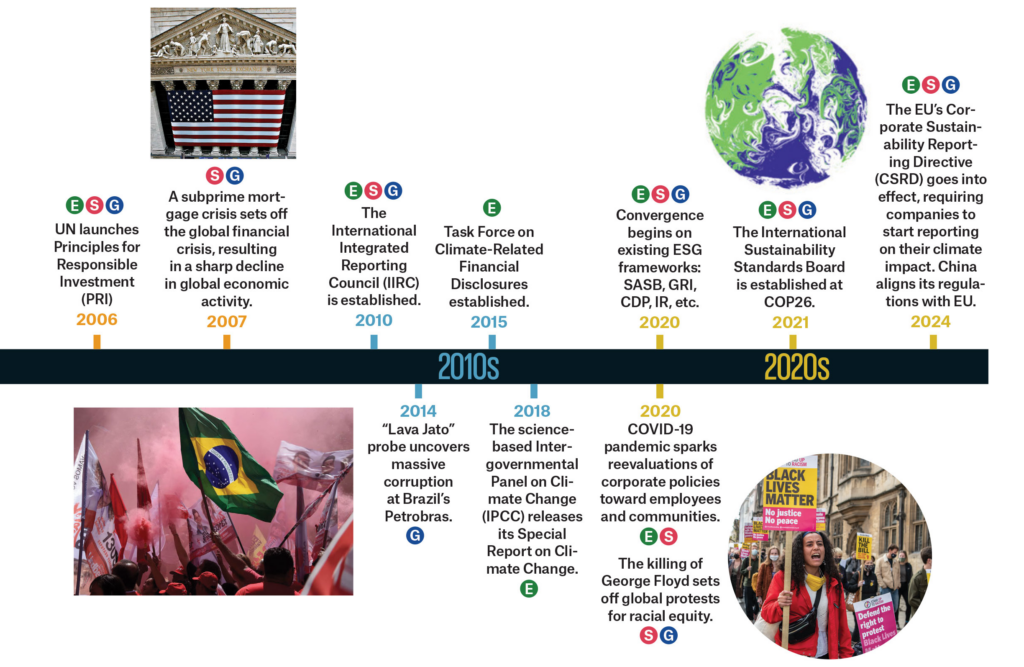

Damaging financial collapses marked the ensuing decades. The 1997 Asian financial crisis, the collapses of Enron and WorldCom in 2001 and 2002, and the 2007–2008 global financial crisis continued to draw scrutiny and led to greater regulatory oversight, such as the Sarbanes-Oxley Act. They also sparked investor and social activism.

These also led to the development of reporting frameworks to provide more transparency of companies’ exposure to environmental and social risks. A myriad of reporting frameworks arose, including the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), the Task Force for Climate-related Financial Disclosures (TCFD) and, most recently, the International Sustainability Standards Board (ISSB).

Intangible assets have risen from 17% of market cap in 1975 to 90% in 2020.

Impacting the Bottom Line

Over this period, the rise in focus on ESG has correlated with an intriguing shift in the makeup of market capitalization of listed companies. According to research conducted by Ocean Tomo, tangible assets as a proportion of market value of S&P 500 companies have fallen from 83% in 1975 to just 10% in 2020. Conversely, intangible assets have risen from 17% of market cap in 1975 to 90% in 2020.

Clearly, the significance of these intangible assets in company valuations warrants a closer look. Intangible assets are generated from:

HUMAN CAPITAL This is often the most important asset of a company. Attracting and retaining talent leads to greater productivity and lower turnover costs, resulting in lower costs, higher revenues and sustainable returns for shareholders.

INTELLECTUAL CAPITALOrganizations that recognize and invest in intellectual capital create sustainable competitive advantages that are hard to replicate. They are often also better placed to integrate new technologies that can disrupt or improve productivity and profitability.

SOCIAL CAPITALBuy-in from local communities and other stakeholders that are impacted by the company’s operations is critical to maintaining license to operate.

ENVIRONMENTAL CAPITALMinimizing impact to the environment enables companies to maintain licenses to operate and lowers exposure to punitive regulatory charges.

With about 90% of the market capitalization of S&P 500 companies in intangible assets, it is here that value can be created and destroyed most easily by management, hence the increased focus by investors on issues related to human capital, environmental capital, social capital and intellectual capital.

Findings from recent Brunswick interviews with active investors provide further insight into the growing relevance of ESG. While they continue to primarily base their investment decisions on the quality of board and management, and the future financial performance of the company, we found a greater appreciation of the impact that material ESG issues can have on those expectations, and a growing investor appetite for disclosure about material ESG issues and how they are managed.

Those topics with the potential to impact future cash flow and therefore company value were the chief concerns. Increasingly, investors ask questions such as:

• Will poor environmental management lead to regulatory challenges, fines and potentially a loss of license to operate and lower profits?

• Will transitioning mining vehicles from diesel to electric result in lower fuel costs?

• Will strong diversity, equity and inclusion programs improve the workplace environment, and lead to greater employee retention in a talent-constrained market and, hence, lower costs?

• Will inaction on decarbonization lead to higher costs as carbon prices are imposed, and increase the potential for stranded assets?

Pension funds and other investors with long-term investment horizons are particularly interested in understanding the risks associated with companies that externalize costs in order to maximize short-term profit, at the expense of long-term planning. Companies that ignore external ESG costs are perceived to be unsustainable in the long term; highly exposed to regulatory changes, penalties and fines; and at greater risk of damaging reputational shocks. Thus they risk destroying value—particularly in the longer term.

The Evolution of ESG

ESG’s roots reach back at least to the 17th century. This timeline offers a few highlights in the global corporate relationship with environmental, social and governance concerns over the last 40 years.

ESG in the Boardroom:

A Call to Action

With a rise in investor scrutiny, it follows that material ESG factors are no longer peripheral concerns, but are at the heart of business strategy and the board agenda, directly correlated to long-term value creation as well as destruction, resilience and reputation. So how should boards ensure they are on top of ESG?

1. Get the Skills Right

Given the breadth and complexity of ESG issues, it is critical that boards have the diversity of skills and experience needed to evaluate risks and opportunities. Investors are increasingly focused on the board skill matrix and are willing to vote against the election of directors or put forward new directors who have a skill set that is otherwise lacking.

This occurred in 2022 when a relatively small institutional investor, Engine No. 1, put forward three independent director candidates and succeeded in getting majority support for the appointment of the candidates to ExxonMobil’s board—all of whom had diversified energy experience while the incumbents had none.

2. Establish a Fit-For-Purpose Governance Structure

There is a clear trend toward stand-alone board sustainability committees comprising a majority of independent directors and independent chair—elevating the deliberation of such issues to the highest levels of the company. Similarly, board committee charters are increasingly referring to specific ESG factors for consideration. This includes audit committee charters, which often refer to climate change risk; nomination committee charters, which refer to the need to consider sustainability skills and experience in succession planning; and remuneration committee charters, as ESG metrics are increasingly forming part of at-risk pay.

With a rise in investor scrutiny, it follows that material ESG factors are no longer peripheral concerns, but are at the heart of business strategy and the board agenda.

3. Consider the Broader Stakeholder Impact

While shareholders remain a centrally important audience, it is imperative that boards take a multi-stakeholder approach to evaluating sustainability matters that have the potential to impact operations, reputation and value.

An example of the importance of understanding key stakeholders is Rio Tinto’s destruction of two 46,000-year-old caves with significant aboriginal archaeological cultural heritage in 2020. The subsequent fallout led to the company’s CEO and a number of senior executives to resign. A federal government inquiry into the causes of the destruction found that Rio Tinto’s role in the destruction was “inexcusable,” highlighting that just because something is legal, does not mean it is without serious repercussions, or that it is the right thing to do.

4. Integrate Into Strategy

With ESG contributing so much to the value of a listed company, it is vital that material ESG matters are incorporated into corporate strategy. As the board is responsible for the approval of strategy and oversight of its implementation, it is incumbent on it to ensure that ESG risks and opportunities are addressed.

While ESG continues to be the subject of vigorous debate, there should be no doubt about the relevance of material ESG matters to boards and investors. With greater ESG disclosure requirements becoming law, increasingly savvy and knowledgeable investors, and the constant scrutiny of media, regulators and local communities, ESG matters are set to remain a fixture on the board agenda—and integral to any strategy.

Meet the authors

-

Senior Advisor

Sydney

With over 30 years’ experience engaging boards of APAC companies on critical governance issues, Pru is an expert at helping companies build trust through strong… -

Partner

Sydney

One of the founding partners of Brunswick’s Sydney office, Rory advises companies from financial services to tech, healthcare, infrastructure and energy and resources.

More from this issue

The Backlash

Most read from this issue

The Investor Case

The Resilience Imperative

You might also like

Future Safe

Better Together