Shamina Singh, President of Mastercard Center for Inclusive Growth, talks to Brunswick’s Jon Miller about using data and AI to build an inclusive digital economy.

The workplace is transforming before our eyes as AI drives fundamental shifts in labor markets. Many worry that this shift will worsen economic imbalances and social divisions. But for Shamina Singh, the other side of the coin is more compelling: AI as an engine for prosperity for all.

Singh is the Founder and President of Mastercard Center for Inclusive Growth, Mastercard’s social impact hub. She also serves as Executive Vice President of Sustainability for Mastercard. Under her leadership, the efforts out of the Mastercard Center for Inclusive Growth contributed to Mastercard being named one of Fast Company’s Most Innovative Companies of 2024.

She has held senior positions in the White House and most recently served on President Biden’s Export Council. Currently, Singh sits on the board of The Asian American Foundation, is a Henry Crown Fellow with the Aspen Institute and serves on the advisory boards of Okta for Good and

data.org. She is also a contributor to MIT Sloan Management Review on the topic of Responsible AI.

In a recent interview, Singh shares how the Center for Inclusive Growth is using AI tools and leveraging data to support individuals, entrepreneurs, small and mid-size businesses, and communities around the world. Her goal, she says, is to make sure that the opportunities AI can offer extend to everyone, everywhere.

Why does driving economic opportunity for everyone matter to Mastercard? And what are some of the key challenges?

Mastercard is a technology company that specializes in payments. For more than a decade, Mastercard has prioritized financial inclusion and economic opportunity as a way for more people to transact in the digital economy safely and simply. The more that they engage, the more resilient and prosperous our communities and businesses become.

When we started this work, 2 billion people could not access secure payment methods. Their only choice was to transact in cash, which meant that they were limited in their abilities to conduct day-to-day activities and were much more vulnerable to theft. Things that we may take for granted, like buying a train ticket on our phone, were beyond the reach of too many people. Today, about 75% of adults have accounts. So although many still use cash, the optionality and safety of a digital account will support their growth over time, and at some point, that may help Mastercard.

This commercially sustainable social impact strategy has paid dividends, both for our business and for our impact in the world. We know that by combining philanthropy with business assets, we can extend the life and impact of our work. This approach supports our efforts in bringing 1 billion people into the digital economy by 2025 and why we were able to already bring more than 50 million small businesses into the digital economy.

“This approach supports our efforts in bringing 1 billion people into the digital economy by 2025 and why we were able to already bring more than 50 million small businesses into the digital economy.”

There’s been a lot of discussion about risks that AI might exacerbate economic inequalities and exclusion. What do you think the upsides are? How can it be potentially a force for economic inclusion?

I agree there are risks with AI, but we are optimistic and believe that AI—and tech more broadly—can unlock productivity for workers and small business owners. The risks aren’t unlike those aligned to any technology—the technology isn’t what makes it risky, it’s how that technology is used.

Mastercard has been helping our partners get ahead of the curve for years. For example, our long-standing work in fraud detection is underpinned by our data capabilities, which means customers can trust and be protected by our network.

But, for everyone to benefit from modern technologies, there need to be guardrails around its access and use.

One of the biggest opportunities we saw at the Center was to help build data capacity for social sector organizations, academic institutions, the public sector and even individuals—so everyone can benefit. For example, through Mastercard Strive, we’re helping small businesses understand and navigate the digital and data economy by providing digital support, tools and training through our partnerships with universities like Washington University, Howard University and the University of Chicago. These support education, skilling and training for the next generation of data scientists focused on social impact. We also created data.org, a new fit-for-purpose social sector organization designed to meet the demands of the AI and data economy by building the capacity of nonprofit organizations to realize the power of their own data.

How do you make sure that the benefits of AI are accessible to everyone?

AI has been here for a while. In fact, Mastercard has been using it for a long time. The difference is that today, AI adoption has accelerated across all industries. What I find interesting is that we have a unique opportunity to build incentives into the business model and the technology that creates a competitive race to the top—a race that values data sovereignty and privacy.

One way we are actioning that is by finding and supporting AI solutions from around the world. In June, we announced our first AI challenge, called the AI to Accelerate Impact (AI2AI) Challenge. We targeted organizations, companies and fintechs using AI in positive ways. In December, we announced our cohort of five winners, who will be receiving capital and access to Mastercard resources and expertise. It may not help them achieve hockey stick growth, but our hope is that it could accelerate their ability to grow and scale.

At Mastercard, we are bringing the company’s assets and resources to bear in our efforts. We are working with other companies and governments to replicate the model, using their assets in a way that says, “We have an opportunity here to do something differently that not only helps our bottom line, but also helps the global construct of our work for long-term investment.”

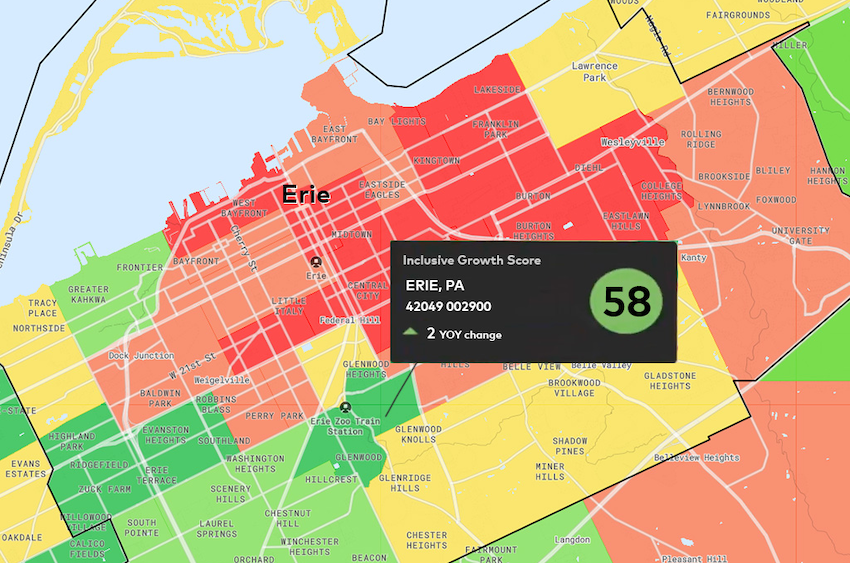

Erie, PA is shown in the Inclusive Growth Score Tool, with lower-scoring census tracts in red, and higher-scoring census tracts in green. The score includes 18 different metrics over six years to show hyper-local changes in neighborhoods across the US.

How does it play out more broadly for smaller businesses, which you mentioned earlier?

AI and data can also be a gamechanger for small businesses. From helping business owners automate their inventory systems, to financial analysis and forecasting, AI can be the tool that gives them the time they need to plan and grow.

However, these technologies also create risks. Fraud and scams are jeopardizing the safety of individuals and growth opportunities of small businesses. For example, according to BlackFog research, 61% of small businesses were the target of a cyberattack in 2022. That’s why it is so important to create solutions that protect individuals and small businesses against these bad actors. In Indonesia, the Center worked with the Global Cyber Alliance (GCA) to translate a Cybersecurity Toolkit to help Indonesian small businesses deal with cybersecurity threats.

Through our Mastercard Strive program, we also provide digital resources and tools to help them build resilience and growth sustainably. When coupled with Mastercard’s AI-enabled card fraud detection technology, which doubles the speed at which it can detect potentially compromised cards, we are providing greater resources that can be applied to protect the entire small business ecosystem.

What are the opportunities to bring value to your customers and partners?

The opportunities are incredible if we have a principled approach. Mastercard operates in over 210 markets, reaching around 100 million businesses and 3.5 billion cardholders. Our network allows us to help move people all over the world from the basics of financial inclusion through to financial security and health. All within a safe and secure system that prioritizes privacy and protection.

All this starts with foundational practices that respect and protect individual rights and society. That is why we developed and continually evolve our Data and Tech Responsibility Principles.

Our baseline belief is that you should own and benefit from your data—and that it’s our job to protect it. We hold ourselves to the highest standards of data and tech responsibility, and these principles inform a broader framework for responsible data-driven innovation.

I’ve heard you speak about the Inclusive Growth Score and the potential around the use of AI for decision-making. Can you talk about that?

Yes, and thanks for making the connection there, Jon. We created the Inclusive Growth Score in connection with the Opportunity Zone incentive established by Congress in the Tax Cuts and Jobs Act of 2017, which sought to encourage long-term investment in various communities across the US.

Anyone can access the tool, it’s free to use and the goal is to help anyone looking to better understand and serve their communities.

The Inclusive Growth Score provides local planners, policymakers, community leaders and impact investors with a clear, simple view of social and economic indicators at the neighborhood level. You could go on InclusiveGrowthScore.com, type in your location and the tool offers an interactive way to visualize the relative economic and social health of every census tract in the US. It looks at things like spend, average income, real estate value, housing affordability, broadband access and more at a census-tract level.

The tool is enormously beneficial for cities that want to attract investment to build out their downtowns, or want to increase shopping rates in a particular market. They can leverage the data to show investors that it’s a good bet.

Anecdotally, we’ve seen impact investors use the tool as an initial assessment of an investment opportunity to determine the economic potential of a place, regardless of whether the overall score is high or low. An example is Erie, Pennsylvania [shown in the image above], where the data is helping pull down investor funding, supporting the case for investment.

AI gives us the ability to ask, “How are we accelerating our decision-making? How are we maximizing the value of every tax dollar of every citizen in the world?” Those kinds of things, to me, are something that, if incentivized correctly, AI has the power to solve.

[You can learn more about the Center’s work at their annual Global Inclusive Growth Summit in DC on April 24. Visit https://globalinclusivegrowthsummit.com/ to learn more.]

Meet the authors

-

Partner

London

Jon left an award-winning career in advertising to help businesses play a more positive role in the world. He is the founder of Open For…

More from this issue

AI Impact

Most read from this issue

The Reporter’s Notebook

An Engine for Prosperity

You might also like

Seeing China Clearly

Leading AI’s Biomedical Revolution